# Total Spillover Indexsp <-G.spillover(VAR_4, n.ahead =10, standardized = F )sp

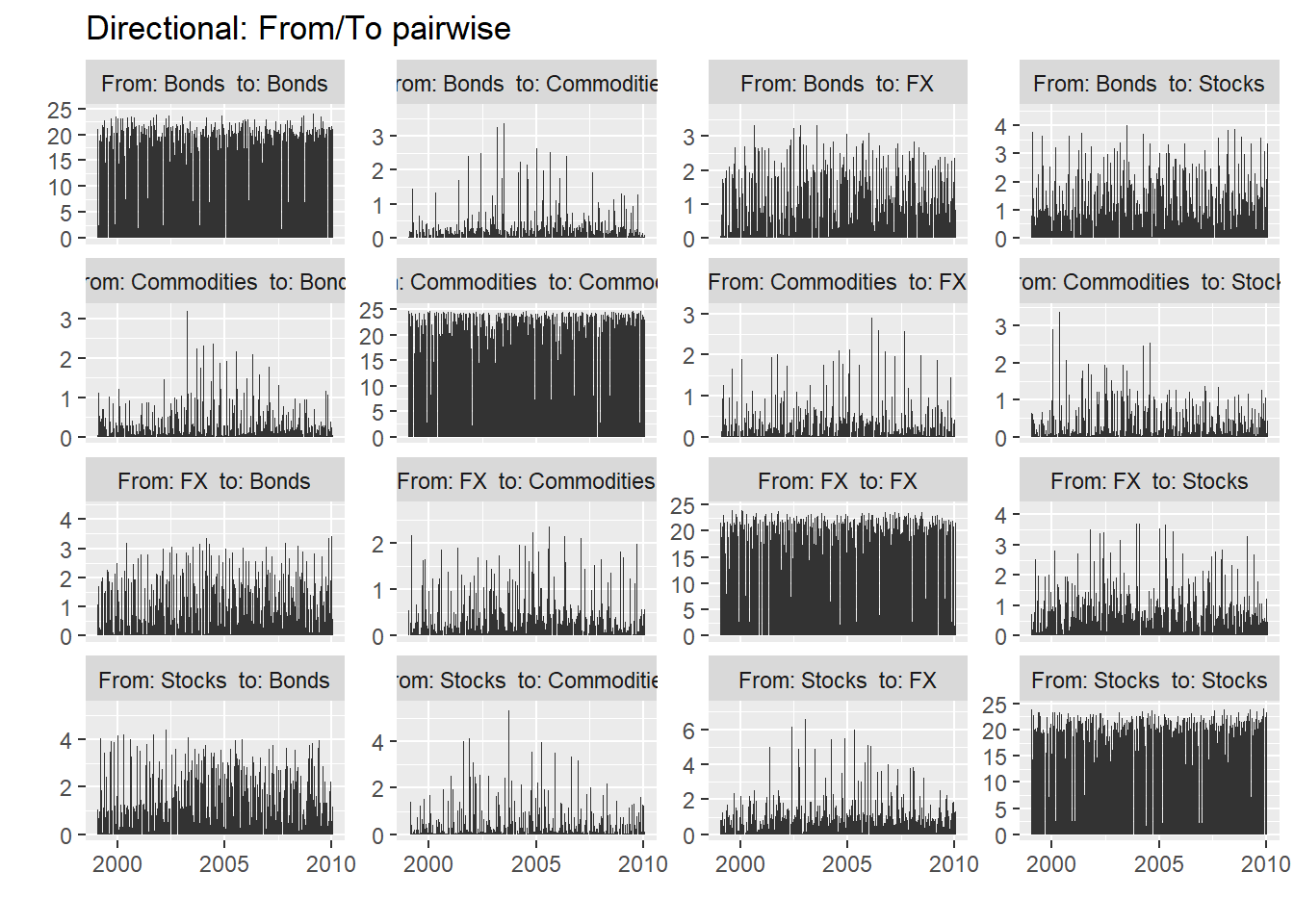

Stocks Bonds Commodities FX

Stocks 88.757002 7.291185 0.3453279 3.606486

Bonds 10.213545 81.445712 2.7269737 5.613770

Commodities 0.468118 3.695953 93.6941893 2.141740

FX 5.691579 7.026017 1.5477592 85.734645

C. to others (spillover) 16.373241 18.013154 4.6200608 11.361996

C. to others including own 105.130243 99.458866 98.3142500 97.096641

C. from others

Stocks 11.242998

Bonds 18.554288

Commodities 6.305811

FX 14.265355

C. to others (spillover) 12.592113

C. to others including own 400.000000

The total volatility spillover appears in the lower right corner of Table, which indicates that, on average, across our entire sample, 12.6% of the volatility forecast error variance in all four markets comes from spillovers

Spillover::net(sp)

Warning in Spillover::net(sp): 'Spillover::net' is deprecated.

Use 'dynamic.spillover' instead.

See help("Deprecated")

To From Net Transmitter

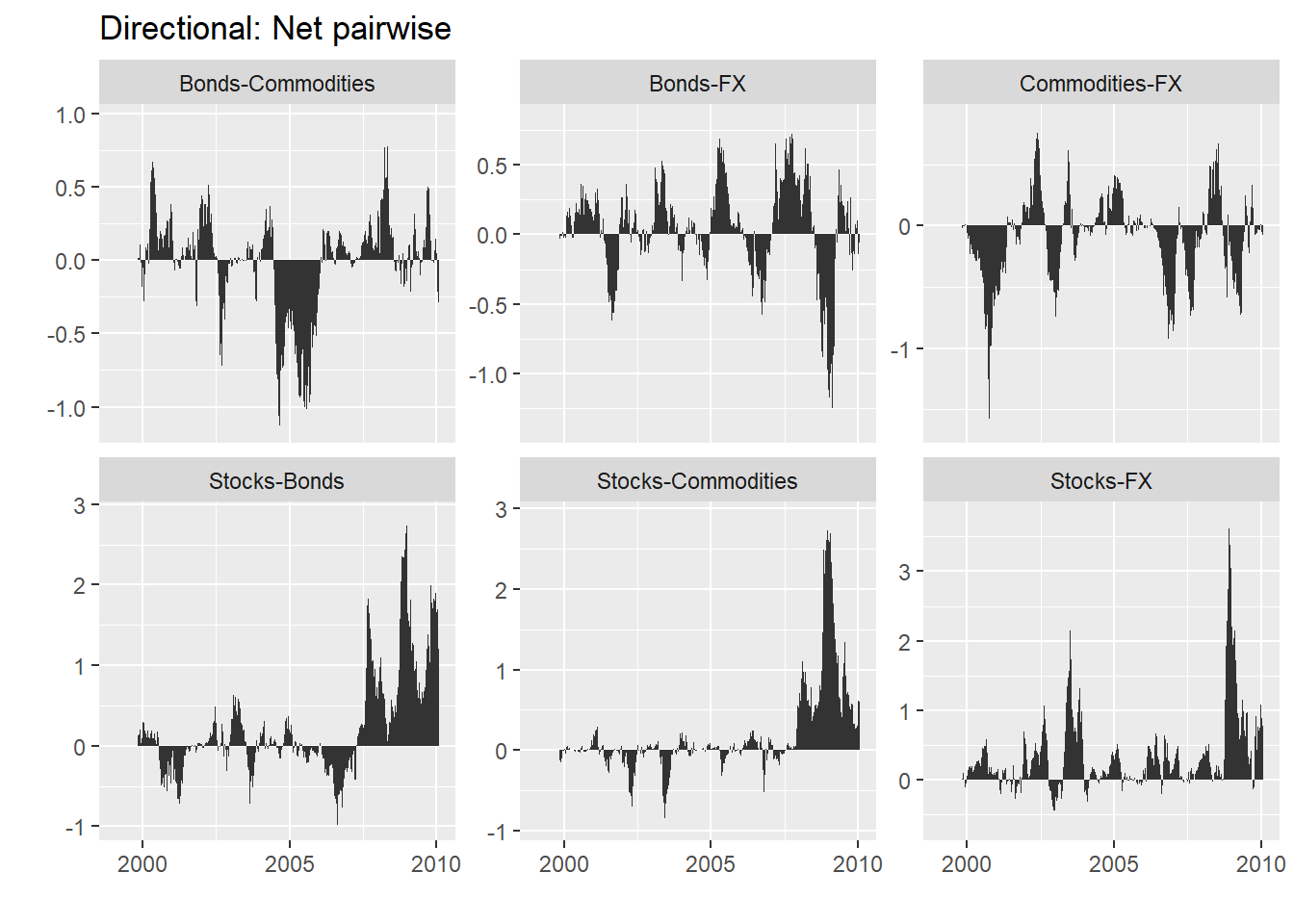

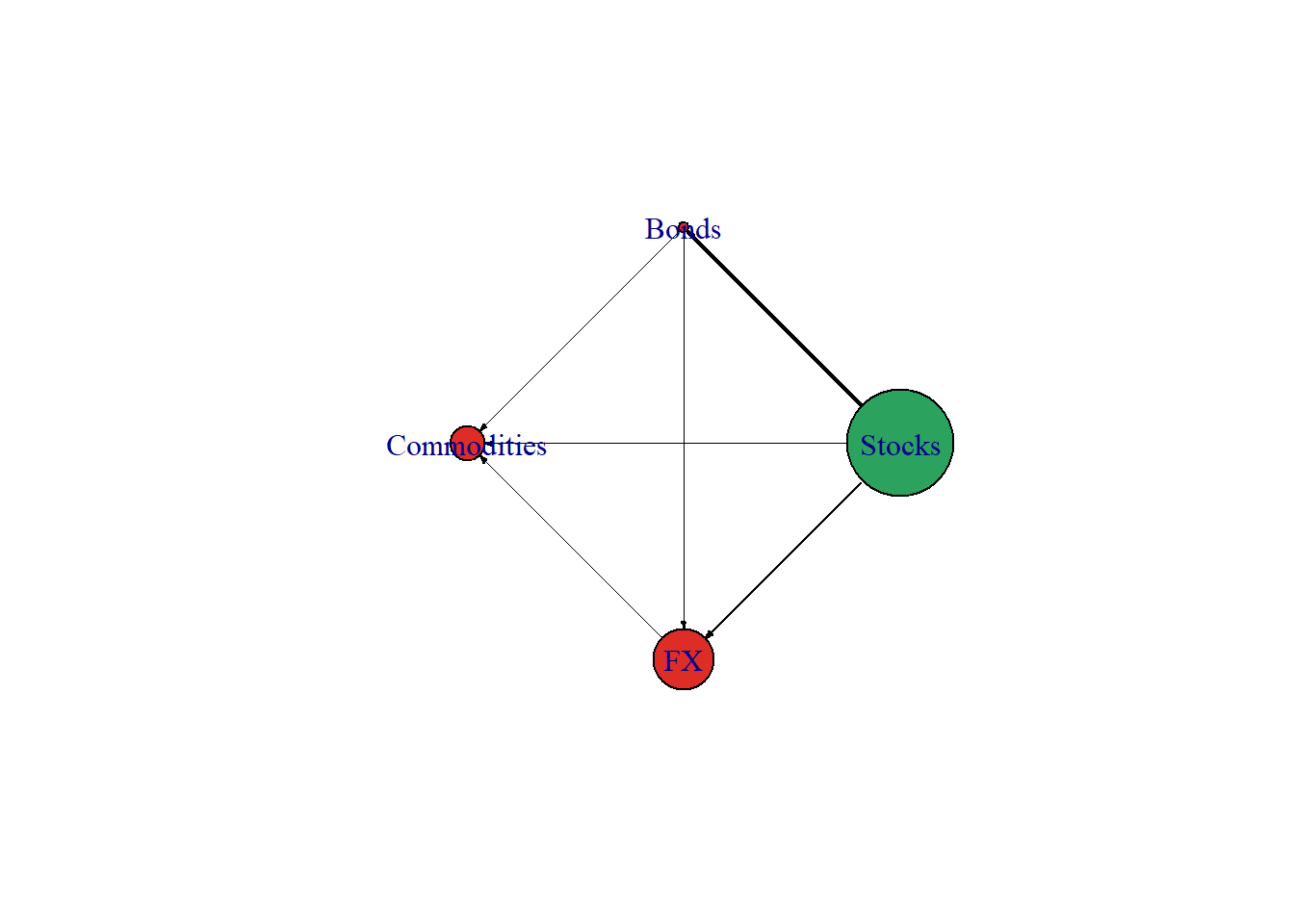

Stocks 16.373241 11.242998 5.1302430 TRUE

Bonds 18.013154 18.554288 -0.5411342 FALSE

Commodities 4.620061 6.305811 -1.6857500 FALSE

FX 11.361996 14.265355 -2.9033588 FALSE

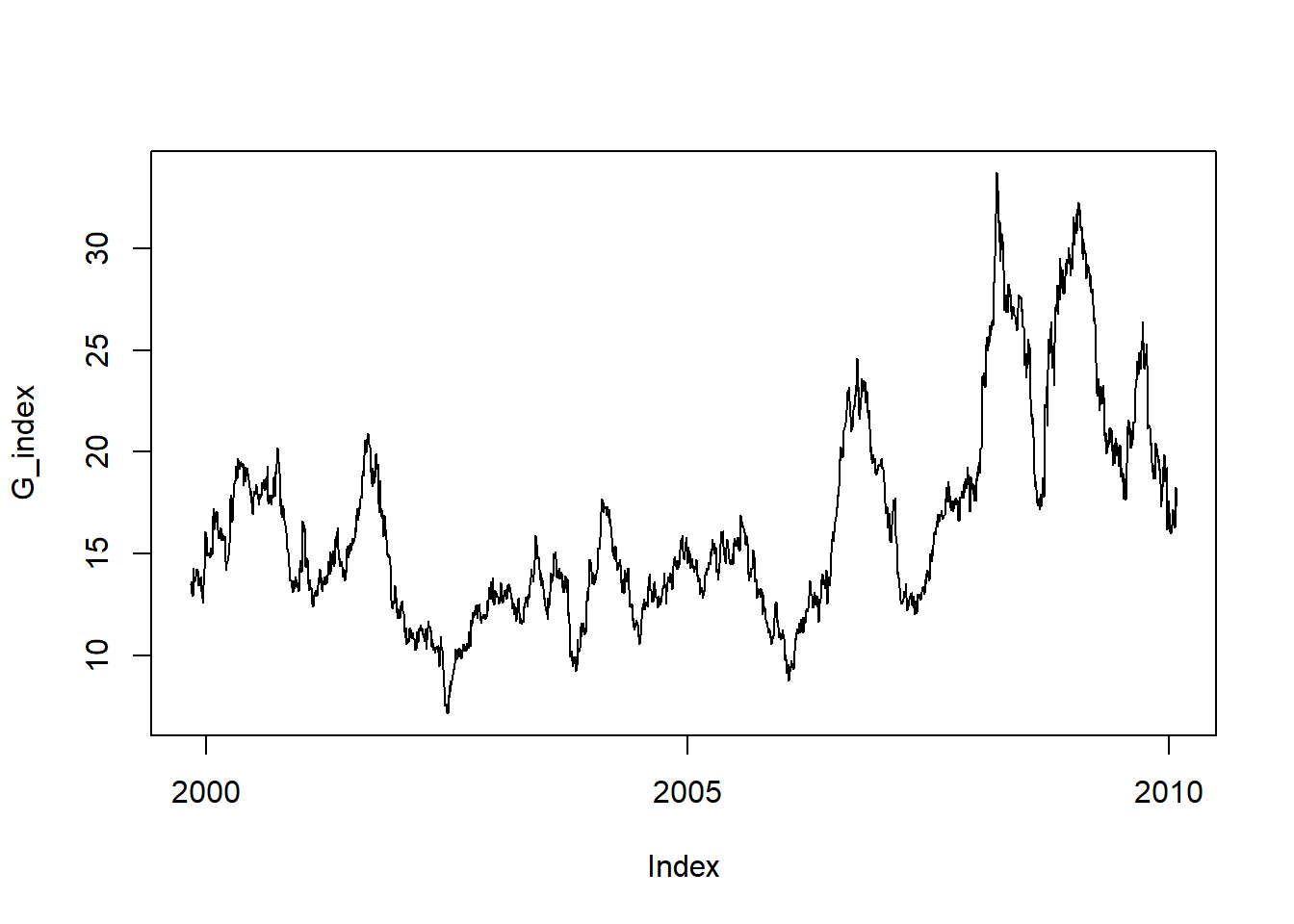

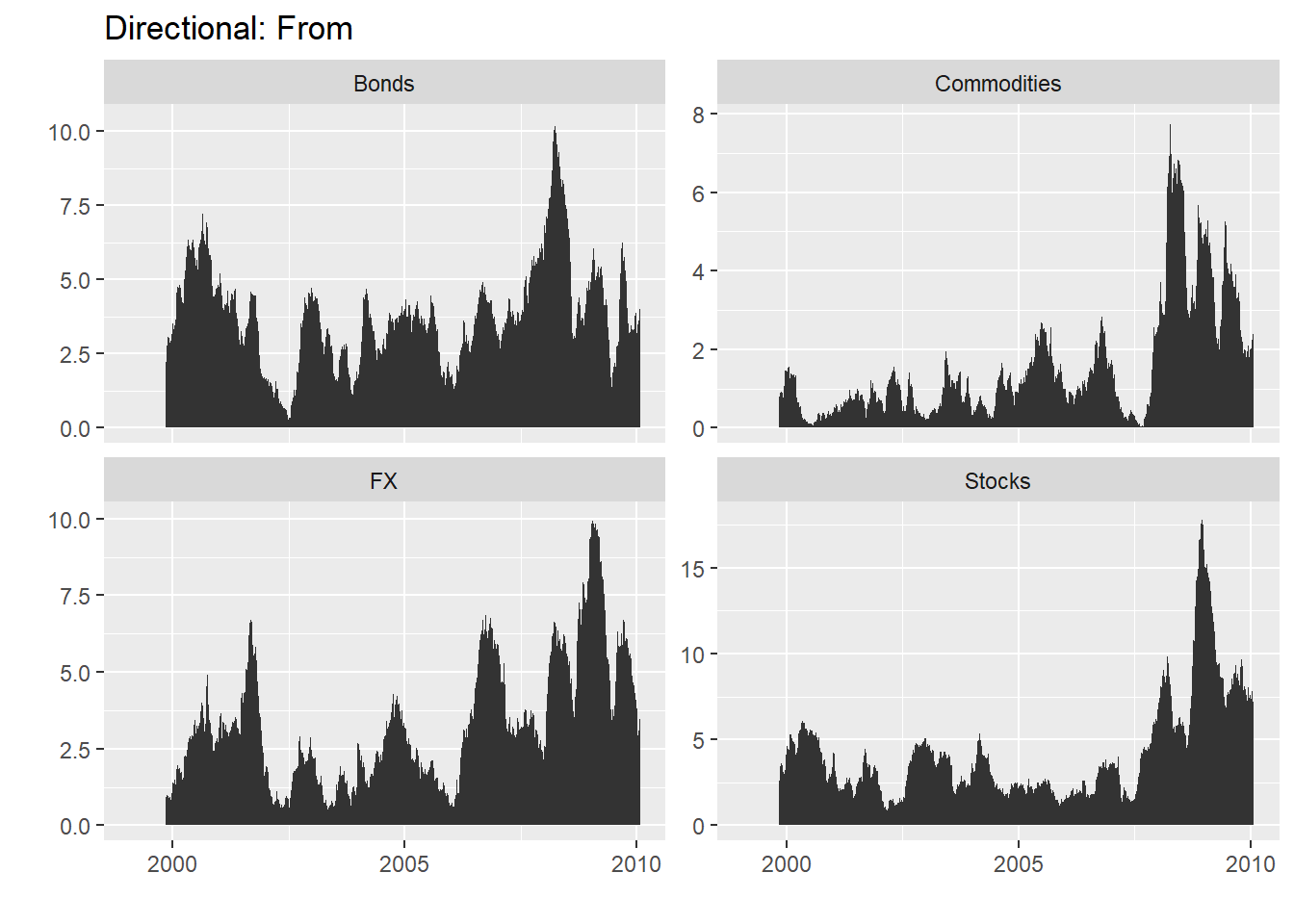

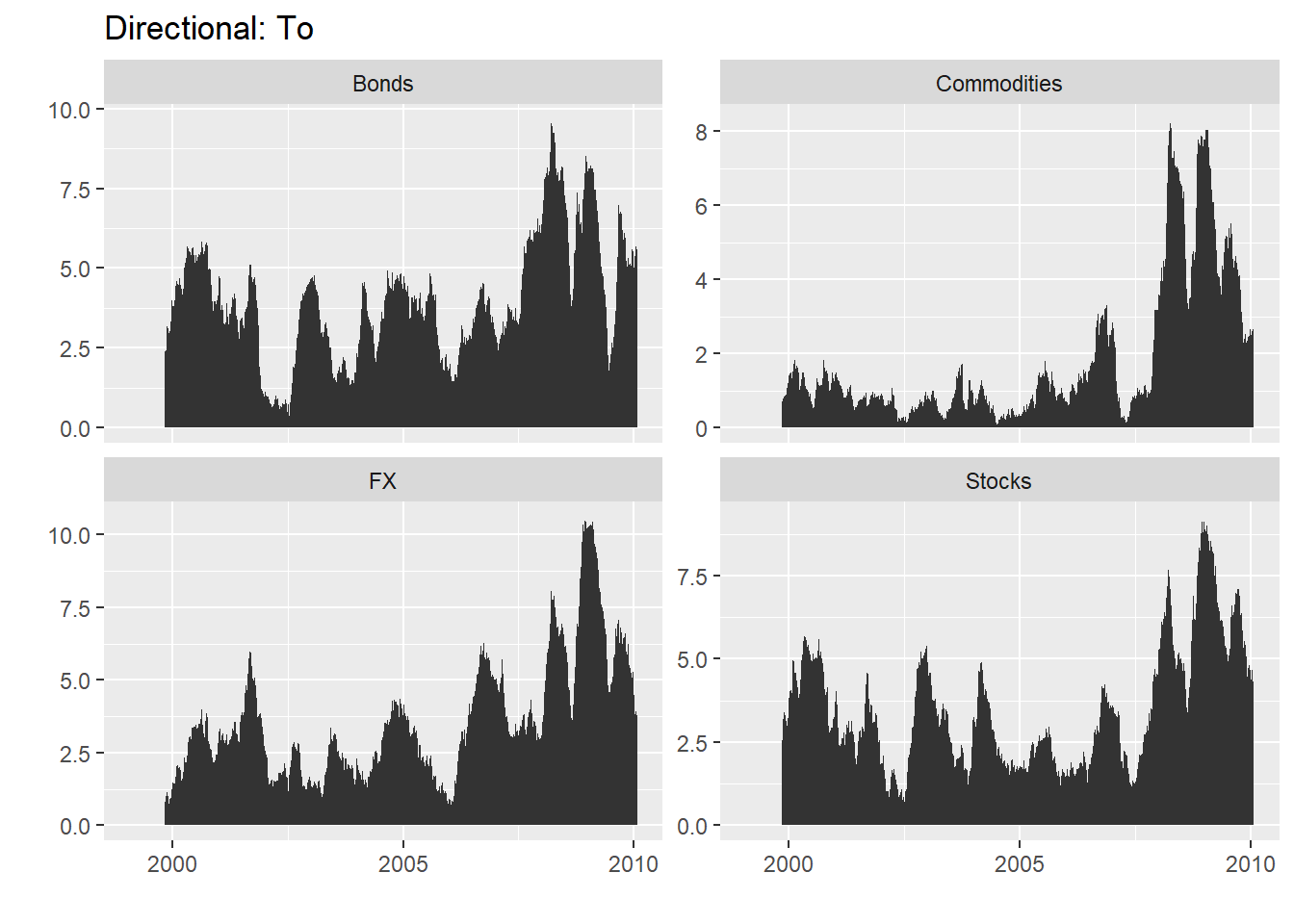

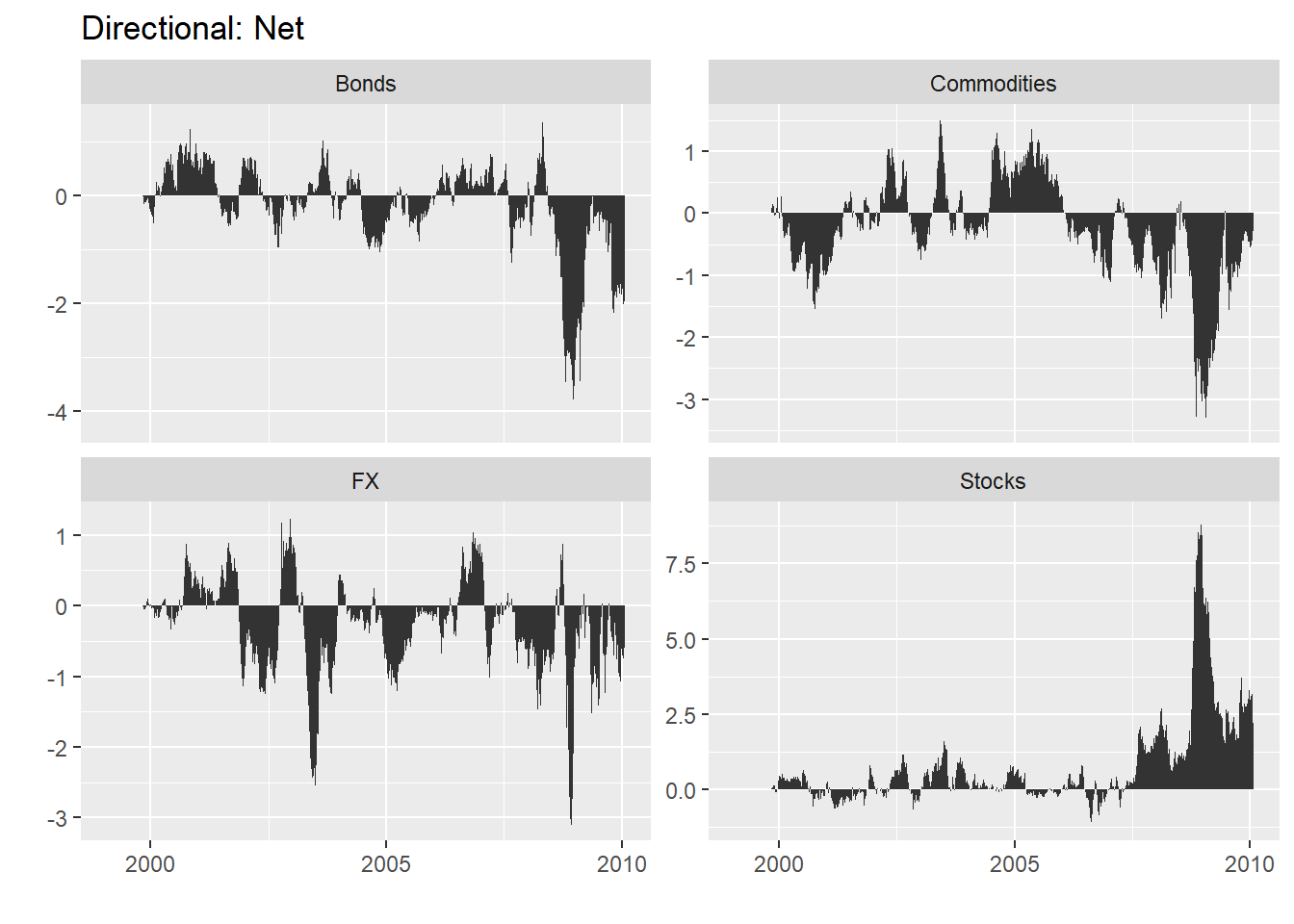

7.5 Dynamic Spillover Index / rolling-sample total volatility spillover

# Data Settingdata(dy2012)dy2012$Date <-as.Date(dy2012$Date, "%Y-%m-%d")dy2012 <-as.zoo(dy2012[,-1], order.by = dy2012$Date)class(dy2012)

[1] "zoo"

# Generalized rolling spillover index based on a VAR(4)G_index<-total.dynamic.spillover(dy2012, width =200, index="generalized", p=4) head(G_index, n=10)