ARIMA(2,1,2)(1,1,1)[12] : Inf

ARIMA(0,1,0)(0,1,0)[12] : 884.0934

ARIMA(1,1,0)(1,1,0)[12] : 872.3993

ARIMA(0,1,1)(0,1,1)[12] : Inf

ARIMA(1,1,0)(0,1,0)[12] : 876.5573

ARIMA(1,1,0)(2,1,0)[12] : 863.6643

ARIMA(1,1,0)(2,1,1)[12] : Inf

ARIMA(1,1,0)(1,1,1)[12] : Inf

ARIMA(0,1,0)(2,1,0)[12] : 867.3178

ARIMA(2,1,0)(2,1,0)[12] : 865.871

ARIMA(1,1,1)(2,1,0)[12] : 865.1084

ARIMA(0,1,1)(2,1,0)[12] : 862.9856

ARIMA(0,1,1)(1,1,0)[12] : 871.9363

ARIMA(0,1,1)(2,1,1)[12] : Inf

ARIMA(0,1,1)(1,1,1)[12] : Inf

ARIMA(0,1,2)(2,1,0)[12] : 861.8543

ARIMA(0,1,2)(1,1,0)[12] : 872.2305

ARIMA(0,1,2)(2,1,1)[12] : Inf

ARIMA(0,1,2)(1,1,1)[12] : Inf

ARIMA(1,1,2)(2,1,0)[12] : 867.0498

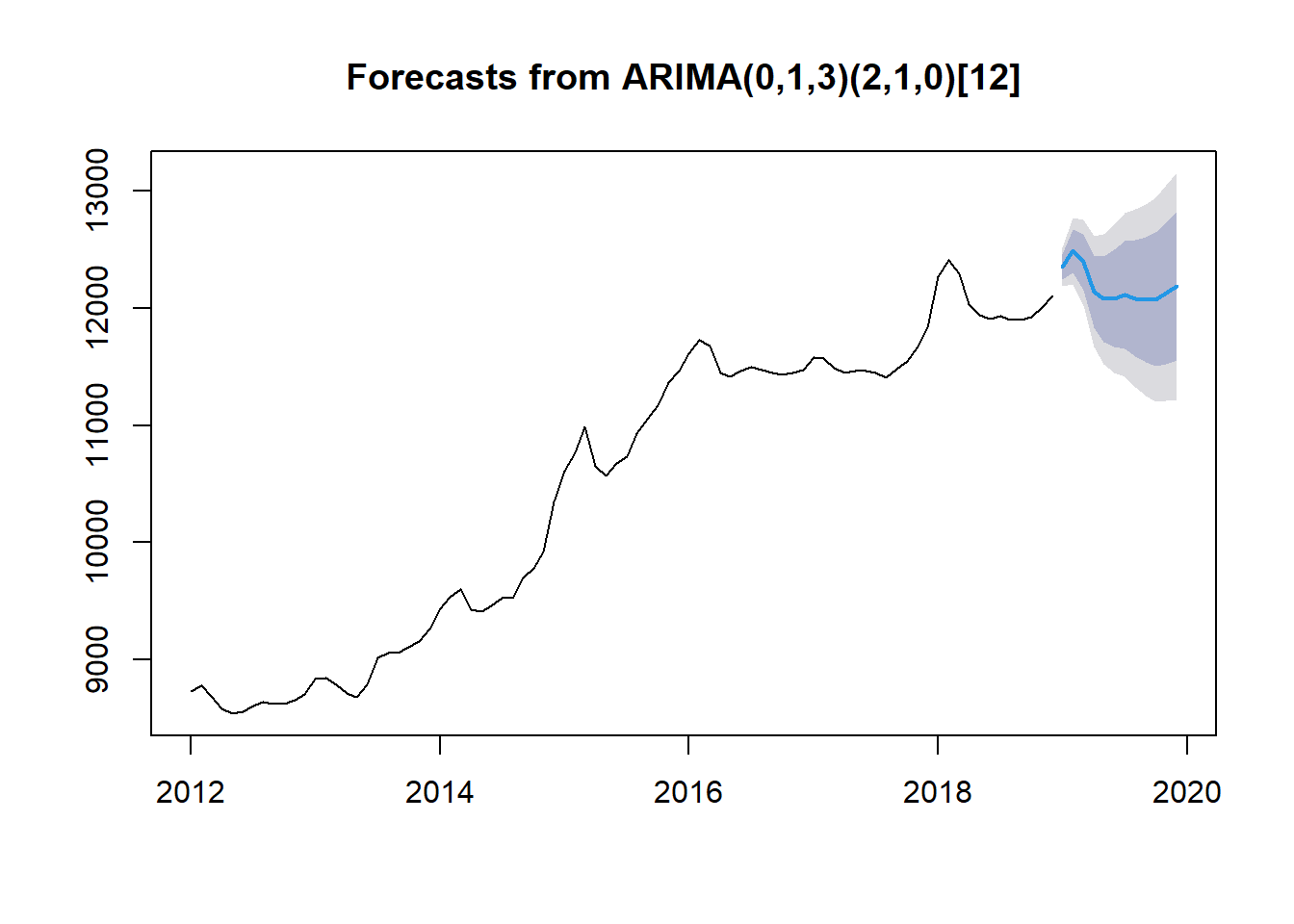

ARIMA(0,1,3)(2,1,0)[12] : 854.8026

ARIMA(0,1,3)(1,1,0)[12] : 865.2557

ARIMA(0,1,3)(2,1,1)[12] : Inf

ARIMA(0,1,3)(1,1,1)[12] : Inf

ARIMA(1,1,3)(2,1,0)[12] : Inf

ARIMA(0,1,4)(2,1,0)[12] : 857.2177

ARIMA(1,1,4)(2,1,0)[12] : 859.7882

Best model: ARIMA(0,1,3)(2,1,0)[12]